Managing your money can feel overwhelming. Bills, groceries, entertainment, and saving for the future can all pile up, leaving you unsure where your money goes each month. That’s why having a clear monthly budgeting strategy is so important. One of the easiest ways to get started is the 50/30/20 budget rule.

The 50/30/20 budgeting rule helps you balance your spending between essentials, lifestyle choices, and saving for the future. Whether you’re completely new to budgeting or just looking for a simple budgeting method, this guide explains everything about the 50/30/20 budget rule, gives real-life examples, and shares tips for putting it into practice.

If you’re just beginning your financial journey, you may also want to explore Budgeting Methods for Beginners, which covers several simple budgeting systems that help people organize their finances and choose the method that works best for their lifestyle.

What Is the 50/30/20 Budget Rule and How It Works

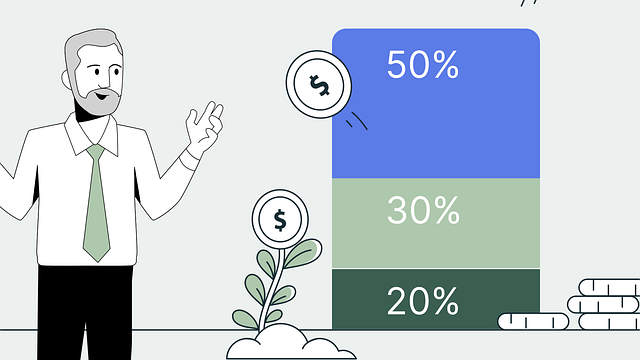

The 50/30/20 budget rule is a framework that divides your after-tax income into three main categories. The percentages are easy to remember: 50% for needs, 30% for wants, and 20% for savings. This structure ensures that you cover essentials, still enjoy your money, and prioritize your financial future.

The beauty of the 50 30 20 rule is its simplicity. Unlike complicated budgeting systems, it doesn’t require tracking every dollar or juggling multiple spreadsheets. It’s a simple budgeting method that most people can follow and adjust to their own financial situation.

Breaking Down the 50/30/20 Rule

50% Needs

Needs are the essentials, the things you absolutely must pay for to live comfortably. The 50/30/20 budgeting rule explained highlights that needs should make up about half of your after-tax income.

Examples of needs include:

- Rent or mortgage

- Utilities such as electricity, water, internet

- Groceries

- Transportation costs like gas or public transit

- Insurance premiums

Tip: If your essentials exceed 50% of your income, consider trimming costs or finding ways to increase your income to keep the budget balanced.

30% Wants

Wants are everything that makes life enjoyable but isn’t strictly necessary. The 50/30/20 rule ensures that you still get to enjoy your money while keeping it under control.

Examples of wants include:

- Dining out

- Hobbies and entertainment

- Streaming services or subscription boxes

- Shopping for clothes, gadgets, or non-essential items

- Travel or vacations

Tip: It’s easy to overspend on wants. Keeping them within 30% of your budget lets you enjoy life while still saving and covering essentials.

20% Savings

Savings are crucial for building financial security. The 20% portion of the 50/30/20 budget rule is dedicated to saving and paying down debt beyond minimums.

Examples of savings include:

- Building an emergency fund

- Retirement contributions

- Paying off debt faster than required

- Investing for future goals

Tip: Even if money feels tight, make an effort to contribute to your savings. Automating transfers can help you stick to this portion of the budget.

50/30/20 Rule Example

To illustrate how the 50/30/20 rule example works in real life, let’s assume your after-tax monthly income is $3,000.

| Category | Percentage | Amount |

|---|---|---|

| Needs | 50% | $1,500 |

| Wants | 30% | $900 |

| Savings | 20% | $600 |

Breakdown:

- Needs: Rent $1,000, utilities $200, groceries $250, transportation $50

- Wants: Dining out $300, entertainment $200, subscription services $100, shopping $300

- Savings: Emergency fund $300, retirement $200, extra debt payment $100

This simple example shows how easy it is to allocate your money effectively using the 50/30/20 budgeting rule.

Benefits of the 50/30/20 Budget Rule

Using the 50/30/20 budget rule comes with several advantages:

- Easy to understand and follow

- Flexible, allowing small adjustments for individual circumstances

- Encourages saving consistently without feeling deprived

- Prevents overspending by clearly dividing income into categories

- Beginner-friendly, making it perfect for those new to budgeting

Limitations and When the 50/30/20 Rule Might Not Work

While the 50/30/20 budgeting rule explained is simple, it’s not perfect for everyone.

- High living costs may push essentials over 50% of income

- People with significant debt may need to adjust percentages

- Low-income households may struggle to save 20% right away

- Freelancers or those with irregular income might need a flexible approach

In these situations, it’s okay to tweak the rule while keeping the core idea: balance between needs, wants, and savings.

Adjusting the 50/30/20 Rule for Different Income Levels

High-income earners: Essentials may be less than 50% of income. Increase savings or fun spending proportionally, and maximize retirement contributions.

Low-income earners: Essentials may exceed 50%. Reduce wants or temporarily lower savings. Focus on a starter emergency fund (How to Build an Emergency Fund) and gradually increase savings as income grows.

Irregular income: Freelancers can calculate an average income over several months and allocate percentages based on that average rather than a single month.

Actionable Budgeting Tips

- Automate savings to make the 20% portion effortless

- Track spending using apps or simple spreadsheets

- Review your budget monthly and adjust as needed

- Reduce spending on wants before touching essentials or savings

- Combine the 50/30/20 rule with other methods like debt snowball or saving challenges Budgeting Methods for Beginners.

FAQs

What is the 50/30/20 budget rule?

It’s a method that divides your after-tax income into 50% needs, 30% wants, and 20% savings.

How do I use the 50/30/20 rule?

Track your income, categorize expenses, and allocate percentages accordingly. Automate savings to make it easier.

Can I adjust the 50/30/20 rule?

Yes. Adjust percentages if you have high living costs, debt, or irregular income while keeping the balance principle intact.

Is the 50/30/20 rule good for beginners?

Absolutely. It’s simple, easy to follow, and provides a clear overview of spending and savings.

Can debt payments count as savings in this rule?

Yes. Paying off debt faster than required is considered part of your savings growth.

Final Thoughts

The 50/30/20 budget rule is more than just numbers, it’s a practical framework for managing your money intentionally. It balances essentials, lifestyle spending, and savings, helping you enjoy life today while preparing for the future.

As you begin applying this method, consider focusing on building long-term financial stability. For example, dedicating part of your savings to How to Build an Emergency Fund can help protect you from unexpected expenses.

You can also accelerate your progress by trying structured saving systems such as Saving Challenges That Actually Work, which can make saving money more motivating and easier to stick to.

Start tracking your spending, allocate your income using this method, and watch your financial confidence grow. What small step can you take this month to apply the 50/30/20 budget rule and take control of your finances?