How to plan your money month by month is one of the most practical financial habits you can build, because it shifts money management from reactive to intentional. Instead of finding out where your money went at the end of the month, you decide where it goes at the beginning.

Most financial stress isn’t caused by low income. It’s caused by no plan. Without a monthly structure, even a good income disappears into bills, impulse purchases, and vague intentions to save next month. A monthly plan gives every naira a purpose before it gets spent.

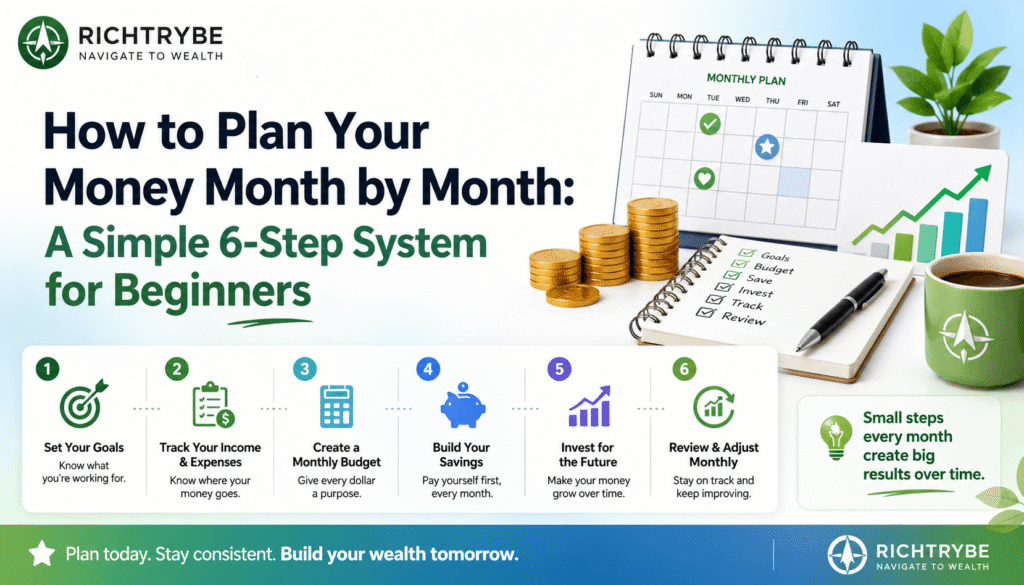

This 6-step system covers everything: calculating your actual income, listing and categorizing expenses, creating a monthly budget, setting priorities, tracking throughout the month, and reviewing at month-end. Each step takes minutes. Together they create the financial clarity that makes progress possible.

Why Monthly Money Planning Matters

Monthly money planning for beginners is the difference between financial control and financial confusion.

Without a monthly plan, you make hundreds of small financial decisions in isolation, each one disconnected from your goals, your budget, and your long-term direction. With a monthly plan, each decision is made inside a structure that already has your priorities built in.

Monthly planning also creates accountability. When you write down where your money should go, you have a reference point to check against throughout the month. That reference point is what catches overspending early and keeps savings on track.

How to Plan Your Money Month by Month: 6 Steps

This 6-step simple monthly money plan works whether you’re just starting out or looking to improve an existing approach. Work through each step in order, the later steps depend on the clarity created by the earlier ones.

Step 1: Calculate Your Monthly Income

Month by month financial planning starts with knowing exactly how much money you have to work with. This sounds obvious, but most people estimate rather than calculate, and estimates lead to plans that don’t fit reality.

Write down every income source: salary, freelance work, business income, side income, and any other regular cash inflow. If your income varies month to month, use an average from the last 3-6 months as your baseline.

Use your take-home amount, not gross income. What you plan with has to match what actually arrives in your account.

Step 2: List All Monthly Expenses

Next, list every expense you expect to pay this month. Divide them into two categories: fixed expenses (rent, loan payments, subscriptions that don’t change) and variable expenses (food, transport, entertainment, personal spending).

Don’t forget irregular expenses that only come up certain months, insurance renewals, car maintenance, school fees, and similar costs that aren’t monthly but still need to be budgeted for. If these aren’t planned for, they become emergencies.

Being thorough with your simple monthly money plan prevents the most common planning failure: creating a budget that doesn’t include real costs.

Step 3: Create Your Monthly Budget

With your income and expenses both written down, now you build the budget: assign a specific amount to every spending category so that all of your income is allocated before the month begins.

A simple framework: 50% to essentials, 20% to savings and investments, 30% to lifestyle. Adjust the percentages to fit your situation, the exact split matters less than having one at all.

The goal is zero-based budgeting: income minus all categories equals zero. Every naira has a job. When money has no assigned purpose, it disappears into unplanned purchases. When every amount is accounted for, you spend intentionally by default.

Step 4: Set Your Monthly Financial Priorities

Within your budget, decide what matters most this specific month. Financial priorities shift: some months you’re focused on building an emergency fund, others on paying down debt, others on reaching an investment milestone.

Setting monthly priorities ensures that progress happens on what matters most, rather than spreading effort evenly across everything. Identify one or two financial priorities per month and make sure your budget reflects them, even if it means temporarily pulling back on something else.

Priorities also give you a reason to stick to the plan. When you know why you’re allocating money a certain way this month, short-term spending temptations are easier to resist.

Step 5: Track Your Spending Throughout the Month

A plan without tracking is just a document. Tracking is what keeps the plan functional throughout the month.

Check in on your spending at least weekly, more often if you’re in an early stage of building the habit of month by month financial planning. Compare actual spending against your budget categories. When a category is getting close to its limit, you know in advance rather than discovering it at month-end.

You don’t need a complex app. A simple spreadsheet, notes app, or even a notebook works fine. Consistency matters far more than the tool you use. For approaches that work well for different styles, read Expense Tracking Methods That Actually Work.

Step 6: Review and Adjust at Month-End

At the end of each month, spend 20-30 minutes doing a full review: compare what you planned vs. what actually happened, identify overspending categories, note what went well, and carry any lessons into next month’s plan.

The monthly review is also where you adjust allocations based on new information. If your food spending consistently runs over, that category needs a higher allocation, not more willpower. The plan should reflect reality, not fight against it.

Over time, these monthly reviews compound into a picture of your financial patterns, the specific areas where money is working and the ones that still need attention.

Monthly Money Planning Tips

A few practices make monthly money planning for beginners significantly more effective:

Plan at the same time each month, the last day of the month or the first of the new one. Making it a fixed calendar event removes the friction of deciding when to do it.

Build in a buffer. Life is unpredictable. Allocating 5-10% of your income to an unplanned expenses category prevents small surprises from breaking the whole budget.

Review last month before planning next month. The patterns from the previous month are the most valuable data you have for making next month’s plan more accurate.

Automate everything possible. When savings and bill payments go out automatically, your plan runs itself for most of the month and you only need to actively manage discretionary spending. For a full automation setup, read How to Automate Your Finances Step by Step.

How to Plan Your Money Month by Month FAQs

How do beginners start planning their money monthly?

Start by tracking your income and expenses, then create a simple plan that covers essentials, savings, and spending.

What is the best way to manage money monthly?

Use a simple system: plan your budget, track spending, and review your finances at the end of each month.

How detailed should a monthly money plan be?

Keep it simple. Focus on major categories like bills, savings, and spending to avoid overwhelm.

Can I plan my money monthly with irregular income?

Yes, base your plan on your lowest expected income and adjust as you earn more.

How long does monthly money planning take?

Usually 30-60 minutes per month, depending on how detailed your system is.

Final Thoughts

Monthly money planning isn’t about restricting how you spend. It’s about making intentional decisions in advance so your money moves toward what actually matters to you.

The 6 steps in this guide, calculate income, list expenses, create a budget, set priorities, track throughout the month, and review at month-end, are all the structure most people need. Do them consistently for 3 months and the process becomes automatic. Do them consistently for a year and the financial results become undeniable.

Start this month. Even an imperfect plan made today is more valuable than a perfect plan that keeps getting delayed.

If you want to complement monthly planning with better daily financial habits, read Daily Money Habits That Build Wealth Over Time for the small daily practices that keep monthly plans on track.