Finding the best way to split your income can feel confusing, especially if you’re not sure where your money should go each month. Without a clear plan, it’s easy to overspend, save inconsistently, and feel like you’re not making real financial progress. Over time, this lack of structure can lead to frustration and uncertainty about your finances.

That’s where using a simple money formula makes a real difference. Instead of guessing or making random decisions, you follow a structured system that tells your money exactly where to go. This gives you clarity and control, you know what to spend, what to save, and how to manage your income effectively every month.

More importantly, this approach helps you build consistency. Rather than starting over each month, you develop a repeatable system that improves your financial habits over time. You begin to feel more organized, confident, and in control of your money.

If you want to set up your finances quickly before applying this strategy, How to Organize Your Finances in One Hour: A Simple 6-Step System to Take Control of Your Money Fast can help you get started

Why You Need a System to Split Your Income

Managing your money without a clear plan often leads to inconsistency and poor financial decisions. When there’s no structure, it’s easy to spend impulsively, forget important expenses, or save whatever is left, if anything is left at all. Over time, this creates a cycle where your money feels out of control.

That’s why having a clear income allocation strategy is so important. It gives your money direction before you spend it, instead of trying to fix things after the fact. With a system in place, every part of your income has a purpose, which makes it easier to stay organized and intentional.

When you understand how to divide your income, you begin to take control of your finances in a more confident and structured way. You:

- Stay in control of your spending

Because you’ve already planned where your money should go, you’re less likely to overspend or make impulsive decisions. - Avoid unnecessary financial stress

Knowing your bills are covered and your priorities are funded reduces uncertainty and anxiety. - Build consistent financial habits

Repeating the same system each month helps you develop discipline and better money habits over time. - Make steady progress toward your goals

Whether it’s saving, investing, or reducing debt, a structured approach ensures you’re always moving forward.

This is why learning how to divide your income properly is essential. It turns money management from something reactive and stressful into a clear, repeatable system that supports your long-term financial success.

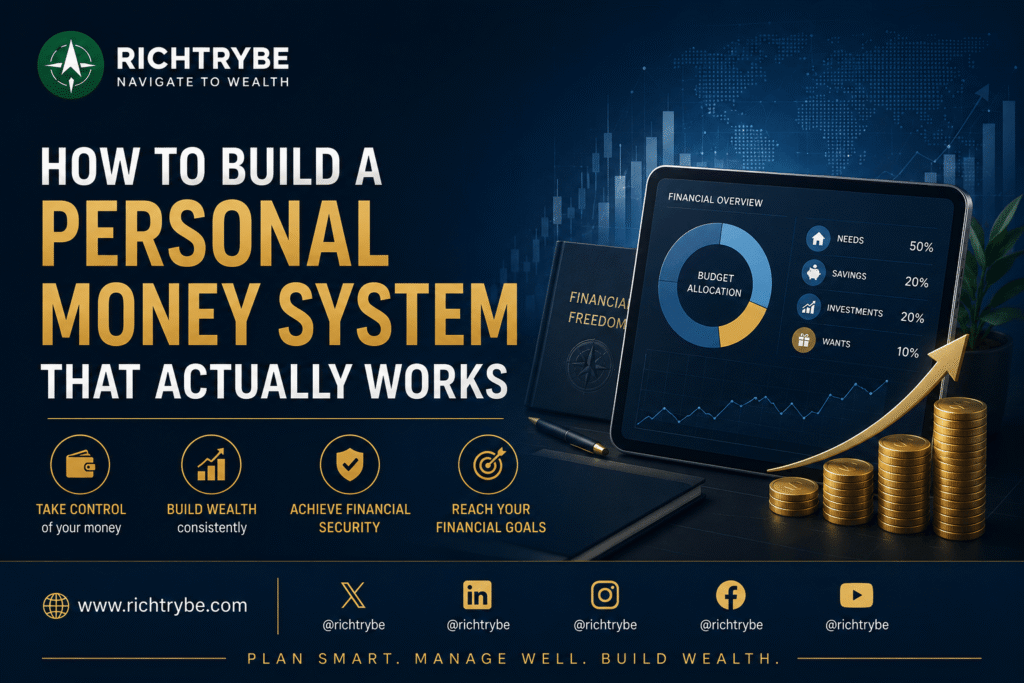

What Is a Simple Money Formula?

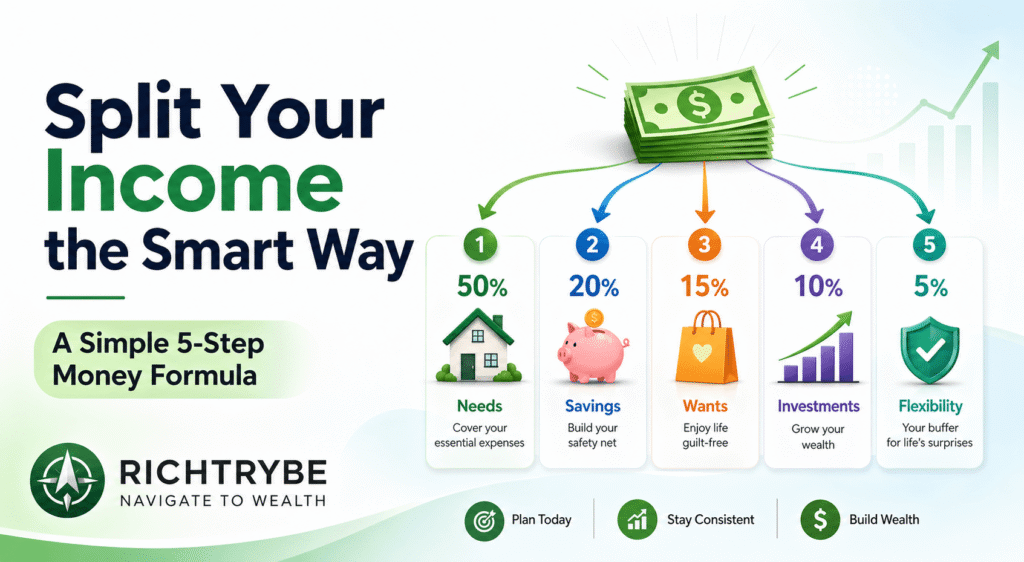

A simple money formula is a structured way to split your income into clear categories like needs, savings, and wants. Instead of spending randomly or trying to manage everything in your head, you use a system that tells you exactly how to allocate your money each month.

The goal isn’t complexity, it’s clarity. A good formula simplifies your financial decisions by giving every portion of your income a specific purpose. This makes it easier to stay organized and avoid common mistakes like overspending or forgetting to save.

One of the biggest benefits of using a simple money formula is that it removes guesswork. You don’t have to constantly wonder if you’re spending too much or saving enough. The structure is already in place, so you can focus on following the plan instead of creating one from scratch every time.

It also makes consistency easier. Once you find a system that works for you, you can repeat it every month with small adjustments when needed. This is especially helpful if you’re learning how to split salary effectively, because it gives you a reliable starting point instead of leaving you overwhelmed.

If you want to build a stronger system around this, How to Plan Your Money Month by Month: A Simple 6-Step System for Beginners shows how to apply this approach in a practical way.

Step-by-Step: The Best Way to Split Your Income

Splitting your income the right way isn’t about strict rules, it’s about creating a balanced system that covers your needs, secures your future, and still allows you to enjoy your money.

This step-by-step approach gives you a simple structure you can follow every month.

Step 1: Cover Your Essentials (Needs First)

Start by prioritizing your basic living expenses, rent, food, utilities, transportation, and any other necessary bills. These are your non-negotiables, meaning they must be paid no matter what.

By handling your essentials first, you ensure stability in your daily life. You avoid situations where important bills are missed because money was spent elsewhere. This step forms the foundation of how to divide your income effectively because it protects your basic lifestyle before anything else.

A good tip here is to calculate exactly how much your essentials cost each month so you always know the minimum amount you need to function comfortably.

Step 2: Allocate for Savings

Once your essentials are covered, the next priority is saving. Instead of saving what’s left at the end of the month, you intentionally set money aside upfront.

Your savings can include:

- Emergency funds for unexpected situations

- Short-term savings for planned expenses

- Long-term goals like education, travel, or major purchases

This step strengthens your income allocation strategy because it ensures you’re building financial security consistently. Over time, even small, regular contributions can grow into something significant.

Step 3: Plan for Investments (If Possible)

If your income allows, the next step is to allocate money toward investments. While savings protect your money, investments help it grow.

You don’t need to start big, even small amounts invested consistently can make a difference over time. The key is consistency, not size.

This step is what moves you from just managing money to actually building wealth. It adds a long-term perspective to your financial plan and helps you prepare for the future.

Step 4: Set Aside Money for Wants

After covering essentials, savings, and investments, you can allocate money for lifestyle spending. This includes things like entertainment, dining out, hobbies, and personal purchases.

This step is important because it keeps your plan realistic and sustainable. Completely restricting yourself often leads to frustration and overspending later.

By intentionally setting aside money for wants, you support how to split salary effectively while still enjoying your life. It creates balance between discipline and flexibility.

Step 5: Leave Room for Flexibility

Finally, leave a small portion of your income unassigned. This acts as a buffer for unexpected expenses or changes during the month.

Life is unpredictable, expenses can come up at any time. Without flexibility, even a good plan can break down quickly.

This is what makes your simple money formula practical and adaptable. Instead of starting over when something changes, you already have room to adjust without stress.

If you want to manage this step better, Budgeting Methods for Beginners: Strategies to Stay in Control of Your Money can help you stay aware of your spending and make quick adjustments when needed.

Simple Tips to Make Your Income Split Work

Having a system is one thing, making it work consistently is what really drives results. The goal is to keep your approach practical so you can stick with it long-term without feeling overwhelmed.

- Keep your system simple and easy to follow

Avoid overcomplicating your income split with too many categories or strict rules. A simple system is easier to manage and more likely to become a habit. - Adjust your allocations as your income changes

Your financial situation won’t always stay the same. As your income increases or decreases, update your allocations so your plan remains realistic and effective. - Stay consistent every month

The real power of any financial system comes from repetition. Even if your plan isn’t perfect, sticking to it each month builds discipline and control over time. - Track your spending regularly

Keeping an eye on your spending helps you stay aligned with your plan. It also allows you to catch small issues early before they turn into bigger problems.

At the end of the day, consistency matters more than perfection. A simple plan you follow regularly will always outperform a perfect plan you don’t stick to.

Common Mistakes to Avoid

Even with a solid system, certain mistakes can reduce its effectiveness. Being aware of them helps you stay on track and get better results from your income split.

- Not saving first

Waiting to save what’s left often leads to saving nothing. Prioritizing savings ensures you’re building financial security consistently. - Overspending on wants

Lifestyle spending can easily get out of control if it’s not planned. Setting limits helps you enjoy your money without disrupting your priorities. - Ignoring small expenses

Small, frequent purchases may seem harmless, but they can quietly drain your budget over time if not tracked. - Using unrealistic percentages

Choosing allocations that don’t fit your income or lifestyle makes your plan hard to maintain. Your system should work for you, not against you.

Avoiding these mistakes helps your system stay practical, balanced, and effective over the long term.

How Splitting Your Income Improves Your Finances

When you consistently apply the best way to split your income, you begin to notice real and lasting improvements in how you manage your money. Instead of feeling unsure or reactive, you develop a clear system that guides your financial decisions every month.

Over time, this structured approach creates meaningful changes:

- Better control over your money

You know exactly where your income is going, which makes it easier to stay within your limits and avoid unnecessary spending. - Reduced financial stress

With a clear plan in place, you don’t have to constantly worry about bills, savings, or unexpected expenses, you’ve already accounted for them. - Clear direction for your finances

Every part of your income has a purpose, giving you a strong income allocation strategy that keeps you focused and organized. - Steady progress toward your goals

Whether you’re saving, investing, or managing expenses, your system ensures you’re moving forward consistently instead of staying stuck.

As you continue, these small, consistent actions begin to compound. What starts as a simple income allocation strategy habit turns into stronger financial discipline, better decision-making, and long-term stability.

FAQs

What is the best way to split your income?

The best way is to use a simple system that prioritizes essentials, savings, and spending while leaving room for flexibility.

How do I divide my income as a beginner?

Start by covering needs, then allocate for savings, followed by wants and other priorities. Keep it simple and realistic.

What percentage should I save from my income?

It depends on your situation, but starting with 10–20% is a practical goal for most beginners.

Can I change my income allocation strategy?

Yes, your plan should be flexible and adjusted as your income or expenses change.

How do I split my salary effectively every month?

Use a consistent formula, track your spending, and review your plan regularly to stay on track.

Final Thoughts

Using the best way to split your income doesn’t require complicated rules or strict formulas, it simply requires a clear system and the discipline to follow it consistently. Once you have a structure in place, managing your money becomes less about guesswork and more about intentional decisions.

The more you stick to your plan, the easier it becomes to stay in control of your finances. You begin to understand your spending, prioritize what truly matters, and make smarter choices without feeling overwhelmed. Over time, this consistency builds confidence and turns money management into a natural habit rather than a stressful task.

As the months go by, you’ll notice real progress, not just in your savings or spending, but in your overall mindset. You become more organized, more aware, and more in control of your financial direction.

If you want to take it further, Monthly Money Reset Routine: A Simple 5-Step System to Take Control of Your Finances Every Month shows how to review, refine, and improve your finances regularly so your system keeps working as your situation evolves.