Most people don’t fail at making money, they fail at managing it consistently. They earn, spend, regret, repeat. The problem is not income alone; it’s the absence of a system that tells money where to go before emotions decide for it.

A personal money system is what separates people who are financially stable from those who constantly feel “behind” no matter how much they earn. It is not about being perfect with money. It’s about building structure so your finances don’t depend on motivation, memory, or mood.

Many people struggle financially not because they don’t earn enough, but because they never learn how to stop living paycheck to paycheck.

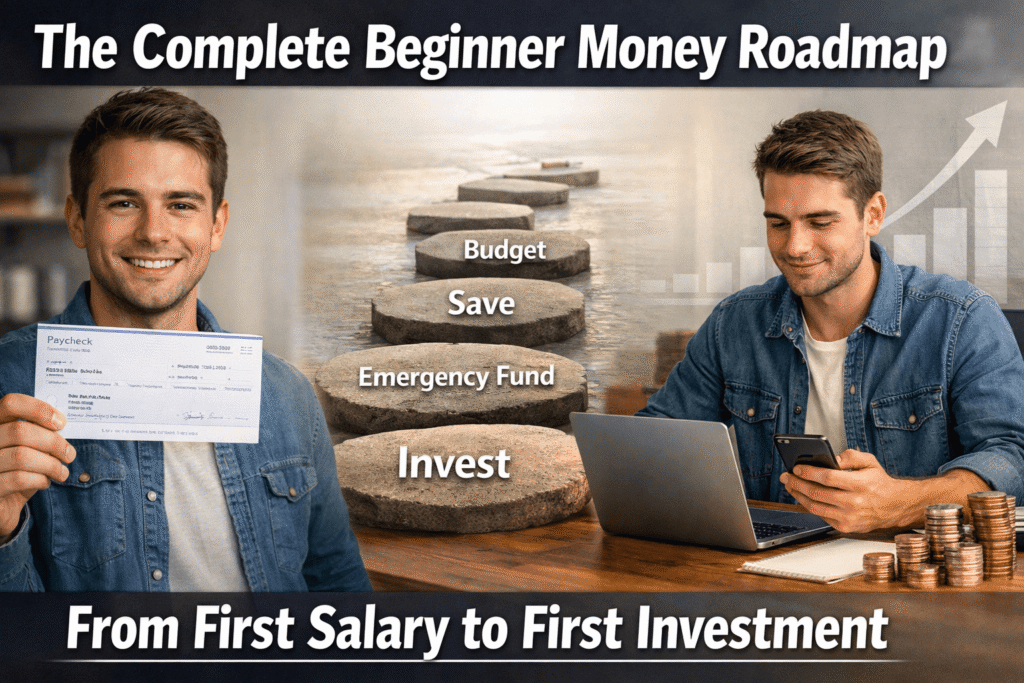

In this guide, you’ll learn how to build a personal money system, even if you’re starting from zero, living paycheck to paycheck, or struggling to stay consistent.

What Is a Personal Money System?

A personal money system is a structured way you manage, allocate, and control your income so that every naira (or dollar) has a defined purpose before you spend it.

Instead of reacting to money problems, you operate with a clear financial framework that answers:

- How much do I spend?

- How much do I save?

- How much goes into investments?

- How do I avoid debt cycles?

- How do I stay consistent every month?

A strong personal finance system removes guesswork and replaces it with rules. Think of it like a “financial operating system” running your life in the background.

Why Most People Don’t Have a Working Money System

A big part of financial struggle is psychological, most people don’t understand the psychology of money habits that influence their spending decisions.

Most people operate without structure. They rely on:

- Memory (“I think I spent too much this month…”)

- Feelings (“I deserve this purchase…”)

- Random budgeting attempts that collapse after a few weeks

This is why most money management systems for beginners fail, they are too complex or not automated.

Here’s what actually breaks most people’s finances:

1. No income structure

Most people treat income as a single pool of money rather than a structured flow. The moment money enters their account, it is seen as “available to spend,” instead of being assigned specific roles.

As a result, money enters their account and gets spent randomly on needs, wants, and impulse decisions without any order or priority. There is no separation between essentials, savings, or future goals.

2. No allocation rules

Without allocation rules, there is no clear breakdown of what money is actually supposed to do. People don’t decide in advance how much should go to savings, expenses, investments, or lifestyle spending.

This lack of structure leads to a situation where money is spent based on urgency or emotion rather than intention. By the end of the month, there is often confusion about where everything went.

3. Emotional spending

A major reason financial systems fail is emotional spending. Purchases are driven by mood, stress, boredom, or impulse rather than planning.

Instead of asking “Does this fit my financial plan?”, most decisions are influenced by how someone feels in the moment. This creates inconsistency and slowly breaks any attempt at financial discipline.

4. No tracking system

Without tracking, money becomes invisible. People often underestimate how much they actually spend because there is no record or review process.

They don’t know where their money actually goes, which makes it impossible to identify wasteful habits, spending leaks, or improvement opportunities. Over time, this leads to financial blindness.

5. No automation

When there is no automation, every financial decision depends on willpower. Savings, investments, and bill payments all rely on remembering and choosing to act consistently.

The problem is that human discipline is unreliable. This means important financial actions are often delayed, reduced, or completely ignored when life gets busy or stressful.

Without a structured system that includes income organization, allocation rules, emotional control, tracking, and automation, financial stress becomes almost inevitable, regardless of how much money a person earns.

A stable financial life is not built on income alone, but on systems that control how that income behaves.

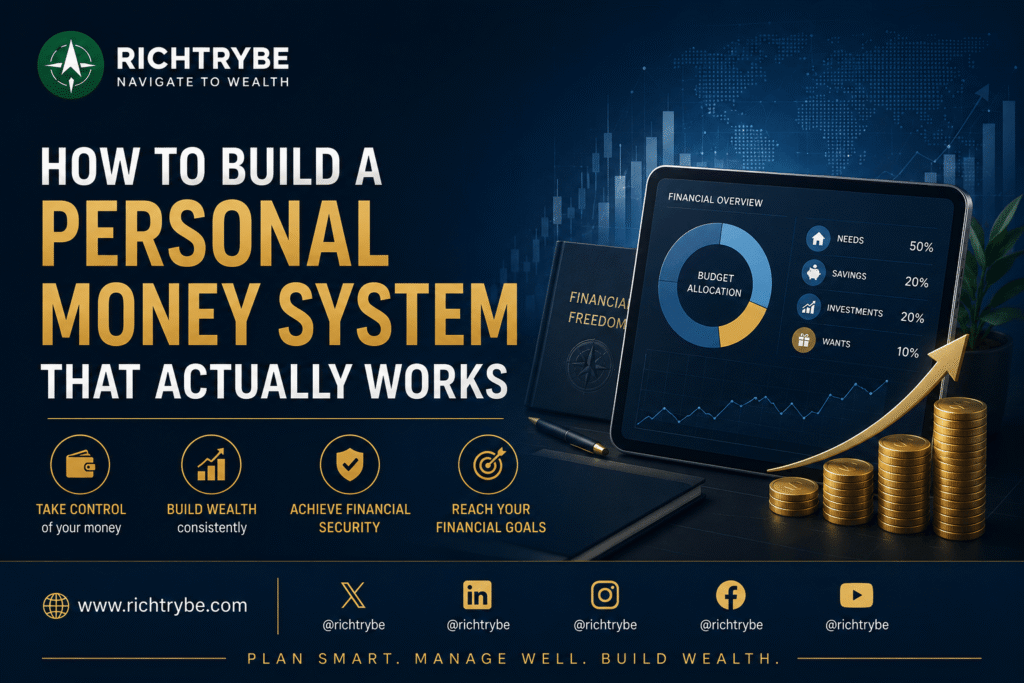

The Core Idea: Your Money Needs a Job

A functional financial system for individuals is built on one principle:

Every unit of income must have a job before it is spent.

This means your money should be divided into categories immediately after you earn it, not after it disappears.

A simple structure looks like this:

- Needs (survival expenses)

- Savings (security)

- Investments (growth)

- Lifestyle (enjoyment)

- Debt repayment (if applicable)

A strong system is the foundation of a personal finance system that helps you stay consistent and in control of your money every month.

How to Build a Personal Money System (Step-by-Step)

Now let’s build your system from scratch. This is the practical framework for creating a personal money system that actually works in real life, not just in theory.

This section will walk you through exactly how to structure your income, apply a personal finance system, and build a simple but effective money management system for beginners that removes guesswork from your finances.

The goal here is to help you move from random spending patterns to a clear and repeatable financial system for individuals, where every part of your money has a defined purpose and direction.

Now let’s break it down step by step.

Step 1: Understand Your Monthly Income Flow

Before you design anything, you need clarity.

Calculate:

- Total monthly income

- Fixed income (salary, business baseline)

- Variable income (freelance, side income)

If you don’t know your numbers, you cannot control them.

This step alone is where many people realize they don’t actually understand their finances.

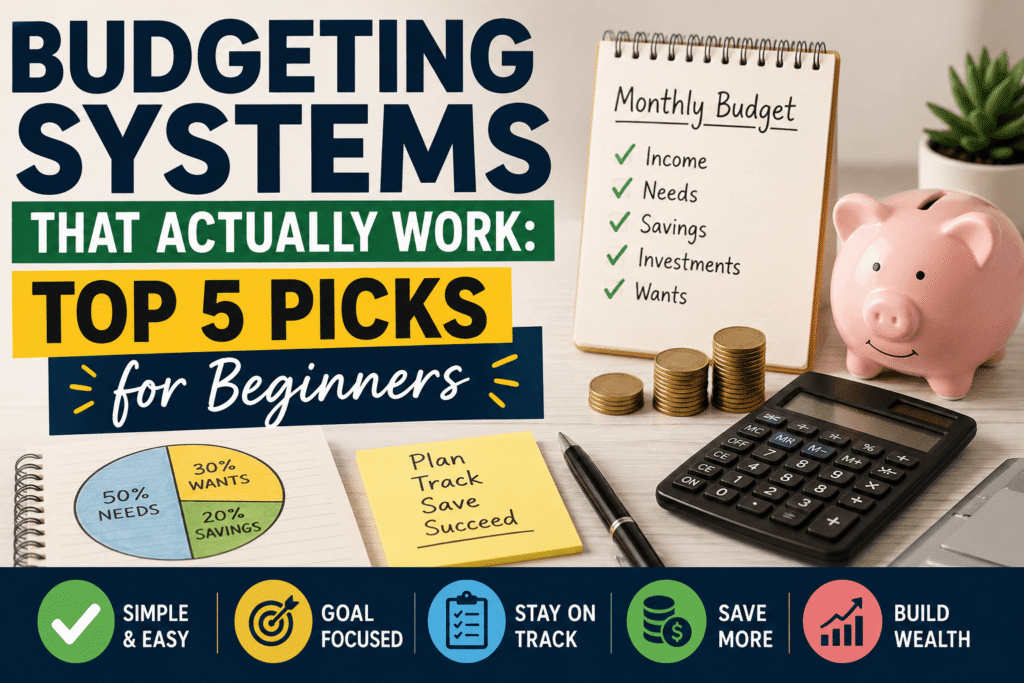

Step 2: Create Your Money Allocation Rules

One of the most powerful ways to stay consistent is learning how to automate your savings system, so saving happens without relying on discipline.

This is the heart of your personal money system.

You assign percentages to your income. A simple beginner-friendly structure:

- 50% → Needs (rent, food, transport, bills)

- 20% → Savings (emergency fund, goals)

- 20% → Investments (stocks, business, skills)

- 10% → Lifestyle (fun, personal spending)

This removes decision-making every month. The system decides, not you.

If your income is unstable, adjust the percentages, but keep the structure.

Step 3: Open “Money Buckets” (Not Just One Account)

One of the biggest mistakes in a money management system for beginners is keeping everything in one account.

Instead, create separation:

- Spending account (daily expenses)

- Savings account (locked or harder to access)

- Investment account

- Bills account (optional but powerful)

This creates friction against impulsive spending.

Even if you use digital banking apps, the principle remains the same: separation creates control.

Structuring your income properly requires understanding budgeting systems that actually work, instead of random or emotional money planning.

Step 4: Automate Everything You Can

A strong system should not depend on discipline alone.

Automation includes:

- Automatic transfers to savings on payday

- Standing orders for bills

- Fixed investment contributions

Automation is what turns a weak personal finance system into a strong one.

If you wait until you “feel like saving,” you will rarely save consistently.

Step 5: Track Your Spending (Without Obsession)

You cannot improve what you don’t track, which is why using expense tracking methods that actually work is essential for financial awareness and control.

You don’t need complicated tools. You just need awareness.

Track:

- Daily spending

- Weekly summaries

- Category breakdowns

You can use:

- Notes app

- Spreadsheet

- Budgeting apps

The goal is not perfection, it is visibility.

A financial system for individuals fails when money becomes invisible.

Step 6: Build an Emergency Buffer First

Before aggressive investing or lifestyle upgrades, build stability.

Your first goal:

- 1 month of expenses → then 3 months → then 6 months

This protects your system from shocks like:

- Job loss

- Medical emergencies

- Income delays

Without this, your system collapses under pressure.

Step 7: Add a Growth Layer (Investments or Skills)

Once your financial basics are stable, the next step is learning how to build wealth from your first salary so your money starts growing instead of just being stored.

Once stability is in place, your system must include growth.

This can be:

- Investing in index funds or stocks

- Starting a side business

- Learning high-income skills

The key idea:

A money system is not just about saving, it is about expansion.

Step 8: Review Your System Monthly

A system that is not reviewed becomes outdated.

Once a month, ask:

- Did I follow my allocation rules?

- Where did I overspend?

- What can be improved?

- Is my income increasing?

This keeps your personal money system alive and evolving.

Simple Money System Framework for Beginners

If you are just starting out, a simple money management system for beginners is the most effective way to build discipline before moving into more advanced financial strategies.

Complex systems often fail at the early stage because they require too much tracking, decision-making, and consistency. What you actually need at the beginning is structure that is simple enough to follow every month without friction.

If everything above feels overwhelming, start with this simplified approach, the 3-Bucket System:

- 70% → Expenses

- 20% → Savings

- 10% → Enjoyment

That’s it.

This beginner-friendly money management system for beginners works because it removes complexity and forces clarity. You always know what percentage of your income goes where, which naturally builds financial discipline over time.

It also helps you develop one of the most important habits in any personal money system, consistency. Instead of guessing or reacting emotionally, your money already has predefined roles every month.

Once you are comfortable and consistently following this structure, you can gradually upgrade into a more advanced personal finance system with automation, investments, and multiple financial layers.

Personal Finance System That Actually Works Long-Term

A long-term working personal finance system is not built on complexity or motivation, it is built on structure that can survive real life.

The goal is to create a system that continues working even when your income changes, your schedule gets busy, or your motivation drops.

A strong system has four key characteristics:

1. Simplicity

If a system is too complicated, it will eventually be abandoned. A good personal finance system should be easy to understand and simple enough to follow every month without confusion or overthinking.

The fewer decisions you have to make, the more consistent you become.

2. Automation

A working system should not depend entirely on discipline. Instead, it should run in the background through automation.

This means setting up automatic savings, transfers, and bill payments so that your financial system for individuals continues working even when you are distracted or busy.

3. Flexibility

Life is not fixed, income changes, expenses shift, and priorities evolve. A strong system must be flexible enough to adjust without breaking.

Instead of rebuilding your entire structure every time something changes, you simply adjust percentages or categories within your existing personal money system.

4. Consistency

Small actions done consistently will always outperform perfect plans that are rarely followed. The real power of a personal finance system is not in its design, but in its execution over time.

Consistency turns your system from an idea into a lifestyle.

At its core, a strong personal finance system is not about strict rules or financial pressure, it is about building repeatable behavior that keeps your money organized, controlled, and growing over time.

Common Mistakes That Break Money Systems

Even well-designed personal money systems often fail, not because the system is wrong, but because of how it is applied. Most people unintentionally sabotage their own progress by repeating a few avoidable mistakes.

Understanding these mistakes is just as important as building the system itself, because avoiding them is what keeps your personal finance system working long-term.

1. Overcomplicating everything

One of the fastest ways to break a money management system for beginners is to make it too complex. People create multiple accounts, excessive categories, and rigid rules that become hard to maintain.

When a system becomes confusing, it stops being used. Simplicity is what keeps financial structure alive.

2. No consistency

A system only works when it is used consistently. Many people start strong for a few weeks, then stop tracking, stop allocating, and eventually fall back into old habits.

Without consistency, even the best personal money system loses its effectiveness over time.

3. Emotional budgeting

This happens when financial decisions are based on mood instead of structure. People adjust their budgets depending on how they feel, spending more when happy, or cutting savings when stressed.

A strong financial system for individuals removes emotion from decision-making by setting rules in advance.

4. Ignoring small expenses

Small expenses often seem harmless, but they are one of the biggest reasons money systems fail. Daily “little” purchases slowly accumulate and disrupt long-term financial goals.

Without proper tracking, these small leaks go unnoticed until they significantly impact savings and investments.

5. No review system

A personal finance system is not something you set once and forget. Without regular review, it becomes outdated and disconnected from your current reality.

Monthly or weekly reviews help you understand what is working, what is breaking, and what needs adjustment.

Avoiding these mistakes is just as important as building the system itself, because they determine whether your personal money system survives in real life or collapses under pressure.

The Real Goal of a Personal Money System

A personal money system is not just about budgeting or tracking expenses. Those are only parts of a much bigger goal. At its core, a system is about changing your relationship with money completely, from reactive and stressful to structured and controlled.

When your personal finance system is working properly, it doesn’t just manage your money; it changes how you think, feel, and behave around money.

A strong system is designed to achieve a few key outcomes:

Removing financial anxiety

Instead of constantly worrying about bills, spending, or “where your money went,” a system gives you clarity. You always know what is coming in, what is going out, and what is being saved or invested.

Creating predictability

One of the biggest sources of financial stress is uncertainty. A well-structured financial system for individuals removes guesswork by giving every part of your income a defined role.

This predictability makes it easier to plan your life, set goals, and make decisions with confidence.

Building wealth consistently

A strong personal money system ensures that wealth-building is not accidental. Whether through savings, investments, or structured income allocation, your system creates consistency, even when motivation is low.

Breaking the paycheck-to-paycheck cycle

Without structure, income is usually spent as soon as it arrives. A system interrupts this cycle by separating money into categories and prioritizing future needs before present desires.

This is what creates long-term financial stability.

When your system is properly built and consistently followed, money stops being something you constantly chase or stress about. Instead, it becomes something you understand, direct, and control with intention.

How to Build a Personal Money System FAQ’s

What is a personal money system?

A personal money system is a structured way of managing income so every part of your money has a purpose, such as spending, saving, and investing, rather than being used randomly.

How do I build a personal money system?

Start by understanding your monthly income, then divide it into categories like needs, savings, investments, and lifestyle. Finally, automate and consistently follow the structure.

What is the best money management system for beginners?

The simplest system is the 3-bucket method:

70% expenses, 20% savings, 10% enjoyment.

It is easy to follow and helps build financial discipline.

Why do most personal finance systems fail?

Most systems fail because they are too complicated or inconsistent. Others fail due to emotional spending, lack of tracking, and no automation.

What is a financial system for individuals?

It is a structured method of controlling income by assigning roles to money before spending it, ensuring clarity and financial stability.

Can I build a personal money system with low income?

Yes. A money system is not about income level but structure. Even with low income, it helps you control spending and build savings gradually.

What is the biggest mistake people make with money systems?

The biggest mistake is overcomplicating the system. Simple and consistent systems always outperform complex ones that are hard to maintain.

How long does it take to build a money system?

You can set one up in a day, but real results come from consistent use over weeks and months.

Final Thoughts

Learning how to build a personal money system is one of the most important financial skills you can develop.

Not because it will make you rich overnight, but because it gives you something far more powerful, control over your money.

And in the long run, control is what actually leads to wealth.

You don’t need a higher income to get started.

You don’t need perfect discipline before you begin.

What you really need is a system that removes pressure from decision-making and makes discipline easier to maintain.

Start simple. Stay consistent. Let the system do the heavy lifting. Then improve it over time as your income, habits, and goals evolve.

That is how real financial stability is built, not through intensity, but through structure that you can stick with.