Two people can earn the same salary and end up in completely different financial positions. The difference usually is not income — it is what each one buys with it. One fills their life with liabilities that drain cash every month; the other builds assets that add to net worth. Learning how to build assets instead of liabilities is really about mastering that single decision, repeated thousands of times.

This guide focuses on the assets-versus-liabilities distinction itself — what truly counts as each, where “good” debt fits, and a simple filter for everyday spending. For the broader case that ownership beats earning, see Why Assets Matter More Than Income.

Quick Answer: How to Build Assets Instead of Liabilities

To build assets instead of liabilities, direct a growing share of your income toward things that put money in your pocket or rise in value, and shrink the share going to things that take money out and lose value. The skill is recognizing which is which before you buy — not after.

Assets vs Liabilities: The Real Difference

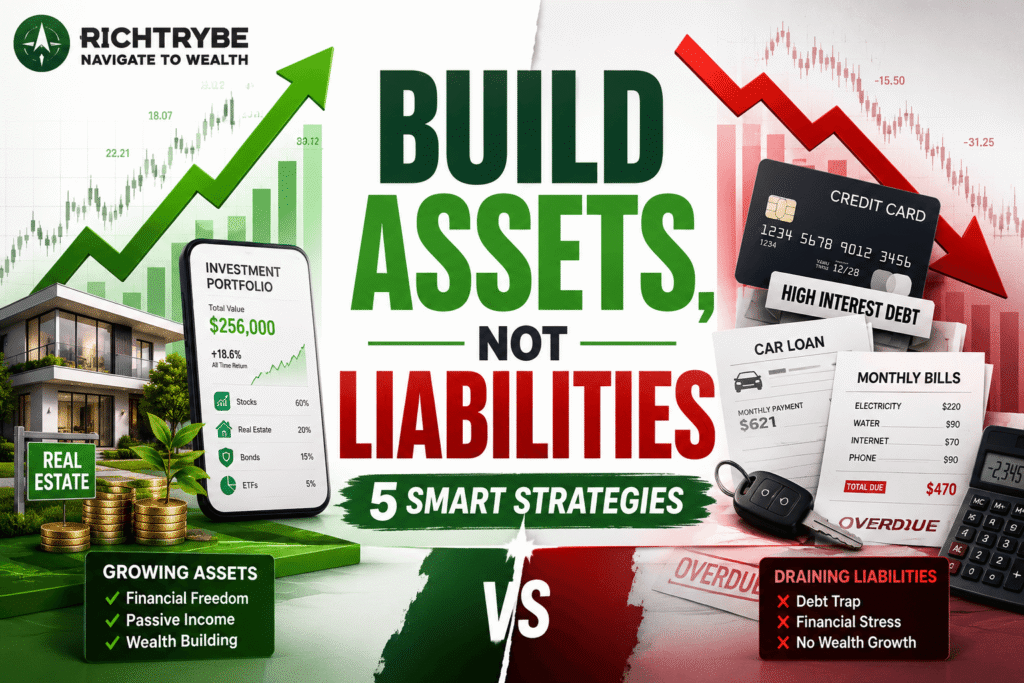

The distinction is simple to state and easy to get wrong in practice. An asset adds to your net worth or generates income. A liability takes money out of your pocket and often loses value over time. Every purchase you make leans one way or the other.

| Feature | Assets | Liabilities |

|---|---|---|

| Cash flow impact | Put money into your pocket | Take money out of your pocket |

| Value over time | Often appreciate or produce returns | Often depreciate or lose value |

| Effect on net worth | Increases it | Decreases it |

| Examples | Index funds, ETFs, rental property, businesses, retirement accounts | Credit card debt, car loans, buy-now-pay-later, luxury purchases |

For the full menu of assets worth acquiring, see The Best Wealth Building Assets for Beginners. The focus here is the other side of the ledger: spotting and controlling liabilities.

Not All Liabilities Are Equal: Good Debt vs Bad Debt

Building assets instead of liabilities does not mean avoiding all debt. Some borrowing can help you acquire an asset that out-earns its cost — the distinction worth learning is between productive and unproductive liabilities.

- Potentially productive: a reasonable mortgage on appreciating property, a business loan that funds profit, or education that raises your earning power.

- Usually unproductive: high-interest credit card balances, financing on rapidly depreciating items, and buy-now-pay-later for consumption.

The test is not “is this debt?” but “does what I am borrowing for build value or destroy it?” A financed car that only depreciates behaves like a liability; a loan that buys an income-producing asset can behave differently.

Why People Accumulate Liabilities by Default

Liabilities accumulate quietly because they feel like progress. A nicer car, an upgraded phone, a bigger lifestyle — each arrives with rising income and feels earned. The problem is that this default direction routes money away from ownership. As discussed in Why Most People Never Build Wealth, prioritizing consumption over ownership is one of the biggest barriers to long-term wealth.

A Simple Filter for Every Purchase

The most practical habit for building assets instead of liabilities is to run larger purchases through one question before buying: “Will this increase my net worth or decrease it?” Replacing the usual question — “Can I afford this?” — with that one quietly redirects money toward ownership over time.

- If it produces income or appreciates → it leans asset; consider it.

- If it only costs money and loses value → it leans liability; minimize it.

- If it is debt → ask whether the thing it buys builds value or destroys it.

You will not pass everything through the filter, and you should not try to. The aim is a steady shift in the ratio — a little more toward assets each year, a little less toward avoidable liabilities. To turn that surplus into actual holdings, see How to Transition From Income to Assets.

The Long-Term Payoff

As the ratio tilts toward assets, the effects compound. Net worth rises, cash flow improves as fewer dollars service debt, financial stress eases, and a growing asset base starts producing income of its own. The shift from consumer to owner is rarely dramatic month to month — but over years it is the difference between a high income and actual wealth.

FAQs

What does it mean to build assets instead of liabilities?

It means directing more of your income toward things that increase your net worth or generate income, and less toward purchases and debt that drain cash and lose value.

What is the difference between an asset and a liability?

An asset puts money into your pocket or appreciates in value, increasing net worth. A liability takes money out of your pocket and often depreciates, decreasing net worth.

Is all debt a liability to avoid?

No. Debt used to acquire an asset that out-earns its cost — such as a reasonable mortgage or a business loan — can be productive. High-interest consumer debt is the kind to minimize.

Is a car an asset or a liability?

For most people a personal car behaves like a liability: it depreciates and carries ongoing costs. It only acts like an asset if it directly produces income.

What is the simplest way to start building assets?

Run larger purchases through one question — “will this increase or decrease my net worth?” — and redirect even a small, consistent share of income toward appreciating or income-producing assets.

Final Thoughts

Learning how to build assets instead of liabilities comes down to a single, repeated choice: ownership or consumption. You do not have to get every decision right. You simply have to shift the balance, year after year, toward things that grow your net worth and away from things that quietly shrink it.

Ready to put the surplus to work? Read How to Transition From Income to Assets for the step-by-step process.