Choosing good assets is only half the job. The harder, more valuable skill is deciding how those assets fit together, where you hold them, and how you keep them on track over time. That is what an asset portfolio actually is: not a pile of investments, but a structured system with a target allocation, the right accounts, and a maintenance routine.

This guide shows you how to build an asset portfolio from scratch by focusing on construction and maintenance rather than the asset menu itself. If you first want to understand which assets belong in a portfolio, read The Best Wealth Building Assets for Beginners, then come back here to learn how to assemble them.

Quick Answer: How to Build an Asset Portfolio From Scratch

To build an asset portfolio from scratch, you make five decisions in order: pick a target asset allocation that matches your timeline, choose which accounts to hold investments in, fill each slot with low-cost funds, automate your contributions, and rebalance on a set schedule. Get those five right and the specific funds you choose matter far less than most beginners think.

Start With Allocation, Not Individual Picks

The most common beginner mistake is starting with the question “what should I buy?” The better starting question is “what mix do I want to own?” Decades of investment research consistently show that your asset allocation — the split between stocks, bonds, and cash — explains the large majority of how a portfolio behaves over time, far more than which particular fund you pick within each category.

Your allocation should reflect two things: how long until you need the money, and how much short-term decline you can tolerate without selling. A longer timeline allows a heavier tilt toward stocks, because there is more time to recover from downturns. According to the U.S. Securities and Exchange Commission, spreading money across different types of assets is one of the most effective ways to manage investment risk over the long term.

How to Build an Asset Portfolio From Scratch in 5 Steps

Step 1: Set Your Target Asset Allocation

Before opening any account, decide on a target split. Here are three common starting points beginners use as a reference rather than a rule:

- Aggressive (long timeline, 15+ years): roughly 90% stocks / 10% bonds

- Balanced (medium timeline): roughly 70% stocks / 30% bonds

- Conservative (shorter timeline or lower risk tolerance): roughly 50% stocks / 50% bonds and cash

These are illustrative, not personalized advice. The point is to choose a deliberate target for your asset portfolio and write it down, because every later decision flows from it.

Step 2: Choose the Right Accounts (Asset Location)

The same investment can grow at very different net rates depending on where you hold it. A sensible order for most beginners is to use tax-advantaged retirement accounts first, then a standard taxable brokerage account for anything beyond that. The account is the container; the allocation from Step 1 is what goes inside it.

- Tax-advantaged retirement accounts — usually the first priority

- A taxable brokerage account — flexible, for goals beyond retirement

- A high-yield savings account — for the cash portion and your emergency fund

Step 3: Fill Each Slot With Low-Cost Funds

Now translate the allocation into actual holdings. Most beginners can implement a complete portfolio with just two or three broad funds — a total-market stock index fund, an international stock fund, and a bond fund — rather than collecting dozens of overlapping positions. For a full breakdown of which fund types do what, see The Best Wealth Building Assets for Beginners.

Keep a close eye on the expense ratio of each fund. Small percentage differences in fees compound into large differences over decades, so low cost is one of the few factors genuinely within your control when you build an asset portfolio from scratch.

Step 4: Automate Your Contributions

Set up automatic transfers on payday so investing happens before you can spend the money. Contributing a fixed amount on a regular schedule — sometimes called dollar-cost averaging — removes the temptation to time the market and turns portfolio growth into a background process rather than a monthly decision.

Step 5: Rebalance on a Schedule

Over time, the parts of your portfolio that grow fastest will drift above their target weight, quietly increasing your risk. Rebalancing means periodically selling a little of what has grown and topping up what has lagged to return to your Step 1 targets. Two simple approaches work well for beginners:

- Calendar rebalancing: review once or twice a year on a fixed date

- Threshold rebalancing: rebalance whenever an allocation drifts more than about 5 percentage points from target

Early on, you can often rebalance simply by directing new contributions toward the underweight asset, avoiding any selling at all.

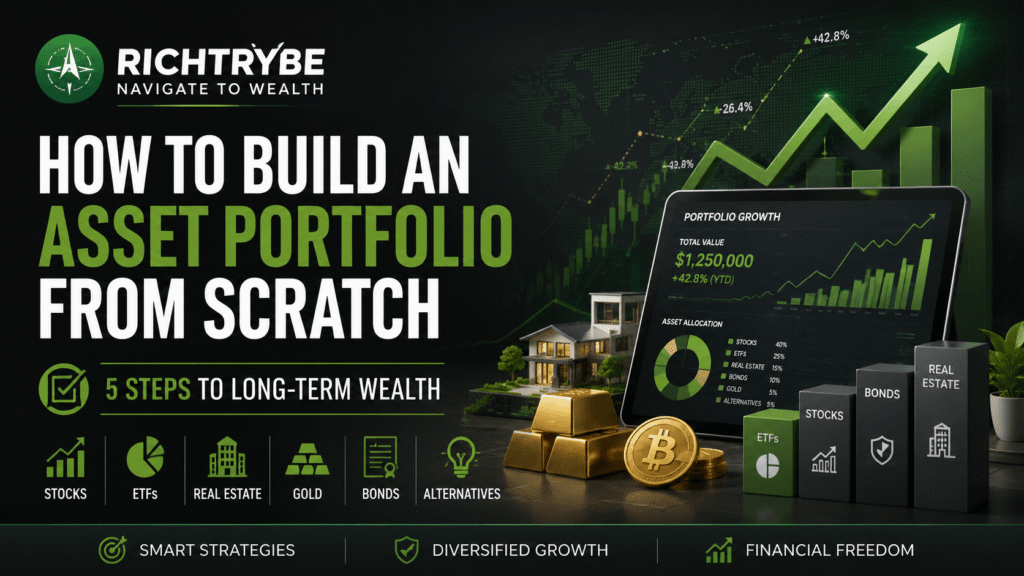

A Sample Beginner Asset Portfolio

To make this concrete, here is what a simple three-fund portfolio at a balanced 70/30 target might look like:

- 50% total domestic stock market index fund

- 20% international stock index fund

- 30% total bond market index fund

This is an example structure for illustration, not a recommendation for your specific situation. The value of a model like this is its simplicity: three holdings, one target, one rebalancing rule. A simple portfolio you actually maintain will almost always outperform a complex one you abandon.

Common Portfolio-Building Mistakes

- Over-diversifying: owning ten funds that all hold the same large companies adds complexity without reducing risk. A few broad funds usually beats a crowded portfolio.

- Never rebalancing: a portfolio left untouched slowly becomes far riskier than intended as winners dominate.

- Performance chasing: constantly swapping into last year’s best performer is a reliable way to buy high and sell low.

- Being too conservative too young: holding heavy cash with a long timeline can cost more in lost growth than market volatility ever would.

- Ignoring fees: high expense ratios and frequent trading quietly erode returns year after year.

For the order in which to actually acquire these holdings as a beginner, see The First Assets Every Beginner Should Focus On.

FAQs

How many funds do I need in a beginner asset portfolio?

Most beginners can build a complete, diversified portfolio with two or three broad index funds. Adding more holdings often increases overlap and complexity without meaningfully reducing risk.

How often should I rebalance my portfolio?

A common approach is to review once or twice a year, or whenever an allocation drifts more than about 5 percentage points from its target. Early on, directing new contributions toward the underweight asset can do the job.

Should I use a retirement account or a taxable brokerage account first?

Many beginners prioritize tax-advantaged retirement accounts before adding a taxable brokerage account, because the tax treatment can meaningfully improve long-term growth. Your own situation and goals determine the right order.

What asset allocation should a beginner use?

Allocation depends on your timeline and tolerance for short-term losses. A longer timeline generally supports a higher stock weighting, while money needed sooner usually calls for more bonds and cash.

Final Thoughts

Learning how to build an asset portfolio from scratch is less about finding the perfect investment and more about creating a structure you can maintain for decades. Set a target allocation, place your assets in the right accounts, keep costs low, automate contributions, and rebalance on a schedule. Those habits do far more for long-term results than any single fund choice.

Ready for the next step? Read The First Assets Every Beginner Should Focus On to learn which assets to prioritize as you begin filling your portfolio.